.webp)

Beyond the Hype

What is Happening ?

In the last two quarters, the narrative surrounding “Data Centers in Space” has reached a fever pitch. The headlines are dominated by a singular use case: Artificial Intelligence. While AI is undoubtedly a catalyst—driving density and power requirements that challenge terrestrial grids ,it is a mistake to view orbital compute solely through the lens of Large Language Model (LLM) training.

At Hypernova we suggest a broader aperture. The “Orbital Data Center” is not merely an AI accelerator in the sky. It is the inevitable evolution of the digital backbone. To understand the investment potential we must deconstruct the demand signal, audit the unit economics and identify the critical hardware bottlenecks.

It’s Not Just AI

To forecast the orbital economy, we must first understand the terrestrial baseline. A data center is a facility designed to store, process, and transmit information. On Earth, the demand for these facilities is heterogeneous.

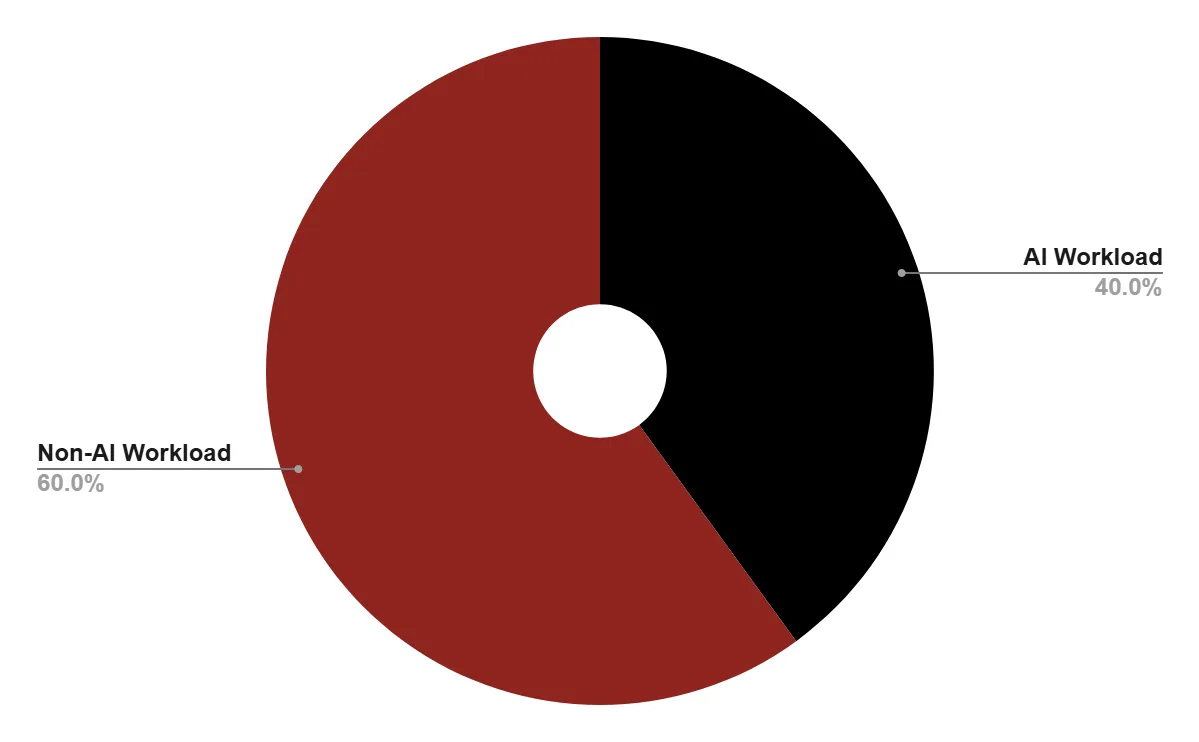

While AI captures 90% of the media attention, it currently represents only 25-40% of the functional demand. As we look to orbit, we anticipate a similar diversification. The killer app for space might not be training GPT-5 — it could be something entirely different.

Unit Economics & The Launch Cost

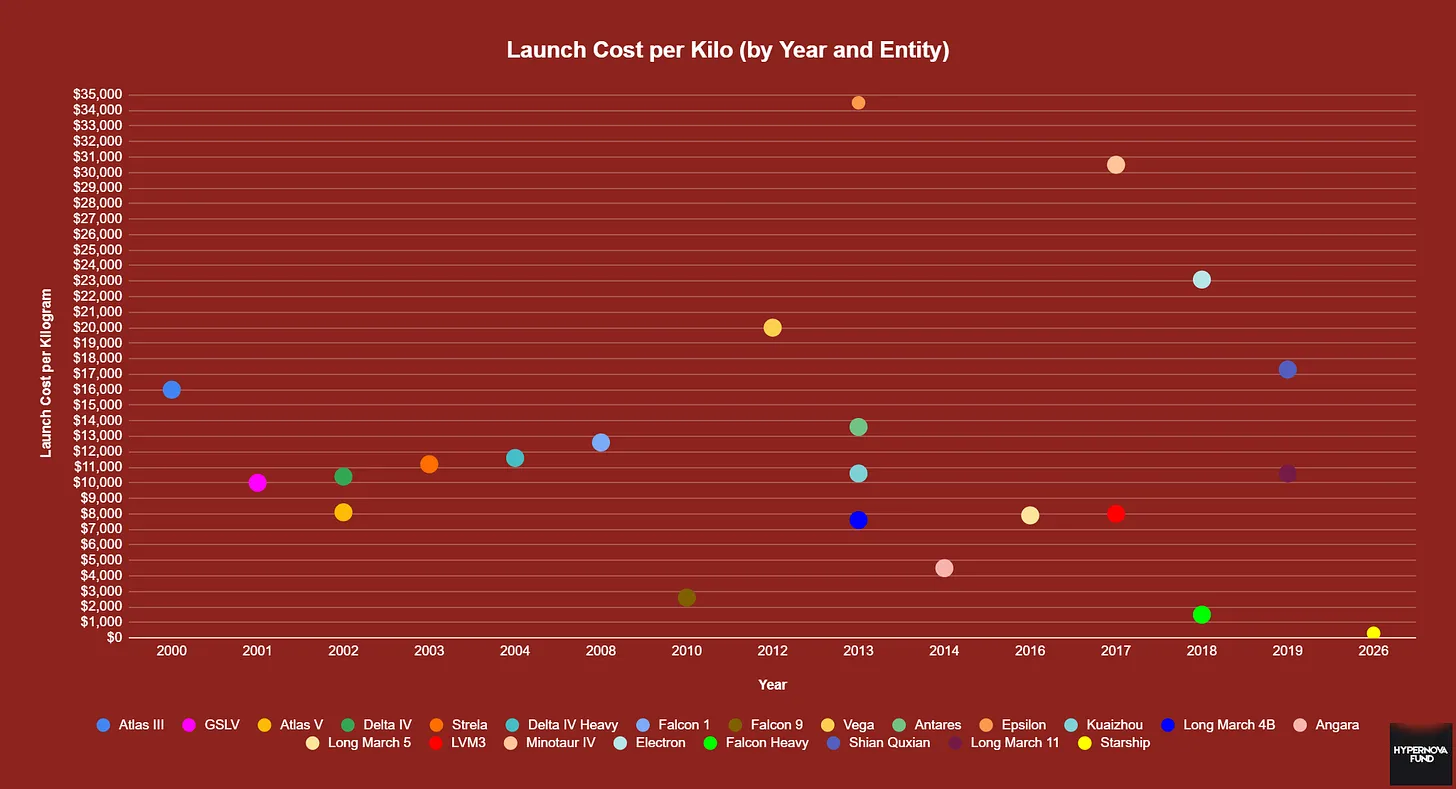

The skepticism surrounding space data centers has historically hinged on cost. However, the introduction of heavy-lift reusable launch vehicles (Starship) is creating a deflationary shock to the launch market.

Let us perform a rigorous “apples-to-apples” cost analysis of deploying a high-performance compute node—specifically a 120 kW rack equivalent to the NVIDIA GB200 NVL72—on Earth versus in Orbit.

With the advent of heavy-lift vehicles like Starship, launch costs are projected to drop to a range of $100–$500 per kilogram. This fundamentally alters the equation for deploying heavy infrastructure.

Contrast this with the capital expenditure (CapEx) required to build equivalent capacity on Earth.

The Solar Hardware Trap

If the analysis stopped at launch costs, the investment case would be undeniable. However, we must scrutinize the Bill of Materials (BOM). The bottleneck has shifted to solar panels; we must also account for the significant costs of thermal radiators for heat dissipation and radiation shielding to mitigate server component failure.

On Earth, solar panels are a commodity, costing roughly $0.30 per Watt. In space, we rely on high-efficiency, radiation-hardened Multi-Junction cells (Gallium Arsenide/Germanium) which are artisanal by comparison.

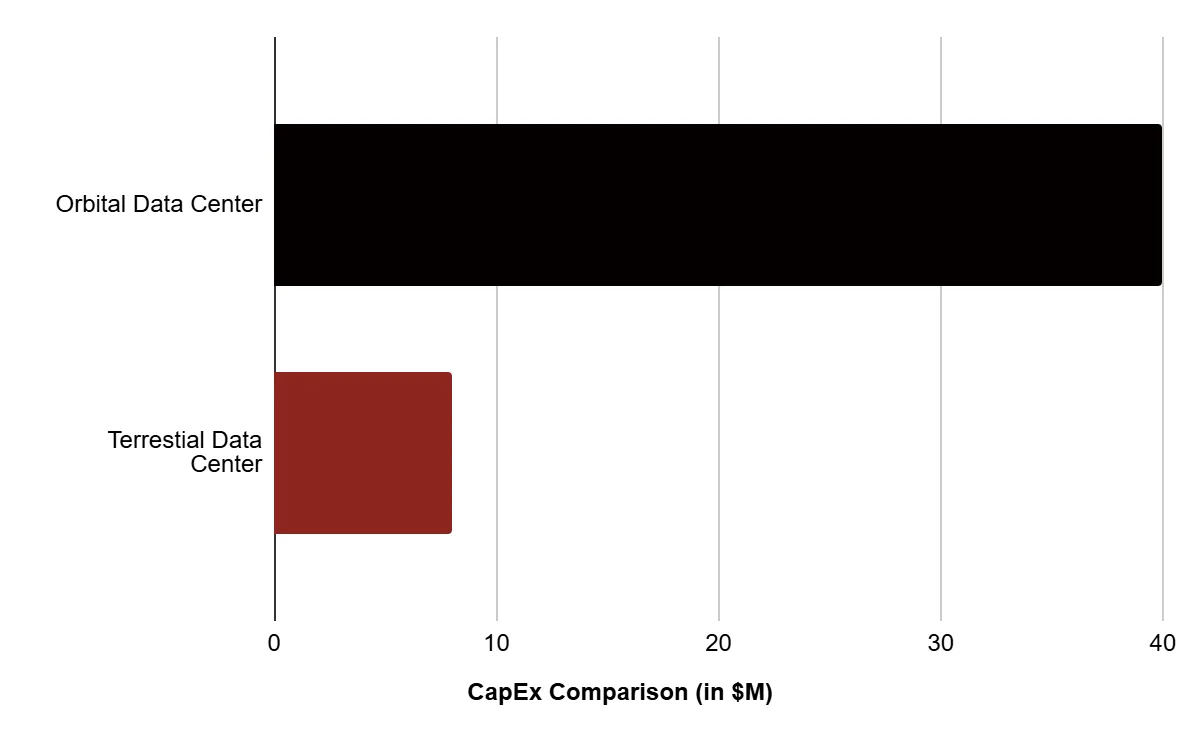

Revised Orbital CapEx:>$40 M (including radiators, cost of build, server rack, launch)

Currently, acquiring a space-based power plant (>$40M) would negate the cost advantages gained from launch and lower energy expenses. As a result, we are evaluating three sectors that are positioned to benefit from the AI-driven expansion while also demonstrating strong, sustainable growth independent of speculative hype.

Edge Compute

The space-based edge computing market, represents a shift from simple data relay to autonomous in-orbit intelligence. By processing data on-board, satellites bypass the critical bottleneck of limited ground station availability. Instead of waiting for a download window to transmit massive raw files to Earth, satellites send only lightweight, critical insights.

This capability is particularly vital for Earth Observation (EO) and on-board image processing, which are expected to capture the lion’s share of the market. Integrated AI allows these orbital nodes to filter vast amounts of visual data in real-time. Ultimately, the strategic advantage lies not in competing with terrestrial networks like 5G, but in solving the scarcity of ground infrastructure capable of receiving and processing raw data.

Data Sovereignty & The “Jurisdiction of Zero”

For global enterprises such as Microsoft or Google, physical jurisdiction presents a significant strategic vulnerability, making the “Jurisdiction of Zero” a compelling alternative for digital asset security. By operating within the vacuum of space, orbital data centers reside outside the sovereign territory of any nation-state, technically insulating assets from unilateral seizure, expropriation, and localized political instability.

This unique legal sanctuary is driving robust demand for space-based storage solutions that prioritize geopolitical neutrality over traditional terrestrial hosting. While the sector experienced a tactical contraction to $1.56 billion in 2025 due to hardware price corrections spikes, a significant resurgence to $1.74 billion is projected for 2026.

Market expansion remains intrinsically linked to infrastructure scaling, with the active orbital fleet expected to exceed 60,000 units by 2030. Sustaining an 11.2% CAGR, the market is forecasted to reach $2.66 billion by 2030, cementing orbital storage as a standardized component of the global digital backbone.

Space Solar Cells

To break the existing cost curve, we are actively tracking innovators like Maana Electric, Redwire, Solestial and others that are revolutionizing space-grade power manufacturing. Alternatively, plummeting launch costs enable a “brute-force” strategy: deploying massive arrays of cheaper, heavier, but less efficient terrestrial-grade silicon panels. While high-performance gallium-arsenide arrays are robust and expensive, cheaper silicon alternatives typically have shorter lifetimes in LEO due to faster radiation degradation.

By leveraging modular designs produced at high economies of scale, operators can achieve the utility-scale generation required for intensive space-based computing. Ultimately, these diverse approaches—ranging from lunar manufacturing to terrestrial-grade brute force—ensure that orbital compute remains economically viable by bypassing traditional terrestrial power and permitting bottlenecks.

The global market for space solar cells is a high-growth sector projected to increase from $1.4 billion in 2025 to approximately $2.4 billion by 2030. This expansion is primarily driven by the mass deployment of satellite constellations, which currently requires the production of high-efficiency cells to power thousands of spacecrafts. Technological dominance is held by multi-junction solar cells, which power over 90% of operational satellites due to their superior performance in harsh, high-radiation orbital environments.

Wrapping up

We posit that orbital data centers will emerge faster than the consensus predicts, as the primary barrier to entry has shifted from Physics to Manufacturing. As launch costs stabilize between $100–$500/kg, the economic gravity of the "Jurisdiction of Zero", low-latency edge compute, cheaper power and new solutions for cooling will inevitably pull high-performance workloads off-world.

The ultimate winners of this cycle will not just be those who launch servers, but the innovators who solve the critical bottlenecks to make orbital infrastructure commercially viable.

Ad Astra !

References

1. JLL, Data Center Outlook: GlobalConstruction Cost Benchmarking and Market Trends, Chicago, IL, 2025.

2. Knight Frank, Global Data Centres Report 2025: Capital, Power, andInnovation, London, UK, 2025.

3. Our World in Data, Cost of Space Launches to Low Earth Orbit,Oxford, UK, 2026

4. Fortune Business Insights, Space-Based Edge Computing Market Size,Share & Industry Analysis, 2021–2034, 2025.

5. Research and Markets, In-Orbit Data Centers Market: Global andRegional Analysis - Analysis and Forecast, 2029-2035, Dublin, Ireland,2024.

6. Grand View Research, Next-Generation Data Storage Market , Share& Trends Analysis Report, 2024–2030, San Francisco, CA, 2024.

7. Grand View Research, Space-Based Solar Power Market Size, Share& Trends Analysis Report By Application, By Region, and Segment Forecasts,2024–2030, San Francisco, CA, 2025.

8. QY Research, Global Space Grade Solar Cells Market Research Report 2024,Beijing, China, 2024.

9. Dataintelo, GlobalSpace Grade Solar Cells Market Analysis and Forecast, 2024-2032,Wilmington, DE, 2024.

10. Market.us, GlobalSpace On-board Computing Platform Market By Platform, By Application, ByEnd-User, and Region - Global Forecast to 2033, New York, NY, 2024.